(ABOVE VIDEO) R. Gary Colton, a public information officer with the U.S. Small Business Administration, speaks with media during an October 22 conference call. File video from the days following Hurricane / Tropical Storm Iselle.

NEWS BRIEF

- U.S. Small Business Administration, under its own authority, has declared a disaster for Hurricane / Tropical Storm Iselle. The announcement was made following the October 16 denial of the state’s appeal for a major disaster declaration. FEMA said the event did not meet the criteria for Individual Assistance, although President Barack Obama did sign Public Assistance Disaster Declaration.

- The disaster declaration makes SBA assistance available in Hawaii County. Low-interest federal disaster loans will be available “to homeowners, renters, businesses of all sizes and private nonprofit organizations whose property was damaged or destroyed by this disaster,” SBA says.

- The filing deadline to return applications for property damage is December 22, 2014. The deadline to return economic injury applications is July 22, 2015.

PRIMARY SOURCE

SACRAMENTO, Calif. – Low-interest federal disaster loans are available to Hawaii residents and business owners affected by Tropical Storm Iselle that occurred August 7 – 9, 2014, U. S. Small Business Administration (SBA) Administrator Maria Contreras-Sweet announced today. SBA acted under its own authority to declare a disaster following the October 16 denial of the state’s appeal for a major disaster declaration.

The disaster declaration makes SBA assistance available in Hawaii County.

“The U. S. Small Business Administration is strongly committed to providing Hawaii with the most effective and customer-focused response possible, and we will be there to provide access to federal disaster loans to help finance recovery for residents and businesses affected by the disaster,” said Contreras-Sweet. “Getting our businesses and communities up and running after a disaster is our highest priority at SBA.”

“Low-interest federal disaster loans are available to homeowners, renters, businesses of all sizes and private nonprofit organizations whose property was damaged or destroyed by this disaster,” said SBA’s Hawaii District Director Jane A. Sawyer. “Beginning today, October 22, at 11 am SBA representatives will be on hand at the following SBA Disaster Loan Outreach Center to answer questions about SBA’s disaster loan program, explain the application process and help each individual complete their application,” Sawyer continued. The center will be open on the days and timesindicated. No appointment is necessary.

HAWAII COUNTY

Disaster Loan Outreach Center

Pahoa Community Center

15-2910 Kauhale Street

Pahoa, HI 96778Opens Wednesday, Oct. 22 at 11 am

Mondays – Fridays, 8 am to 4 pm

Closes Thursday, Nov. 6 at 4 pm

Disaster loans up to $200,000 are available to homeowners to repair or replace damaged or destroyed real estate. Homeowners and renters are eligible for up to $40,000 to repair or replace damaged or destroyed personal property.

Businesses of any size and private nonprofit organizations may borrow up to $2 million to repair or replace damaged or destroyed real estate, machinery and equipment, inventory, and other business assets. SBA can also lend additional funds to homeowners and businesses to help with the cost of making improvements that protect, prevent or minimize the same type of disaster damage from occurring in the future.

For small businesses, small agricultural cooperatives, small businesses engaged in aquaculture, and most private nonprofit organizations of any size, SBA offers Economic Injury Disaster Loans (EIDLs) to help meet working capital needs caused by the disaster. EIDL assistance is available regardless of whether the business suffered any property damage.

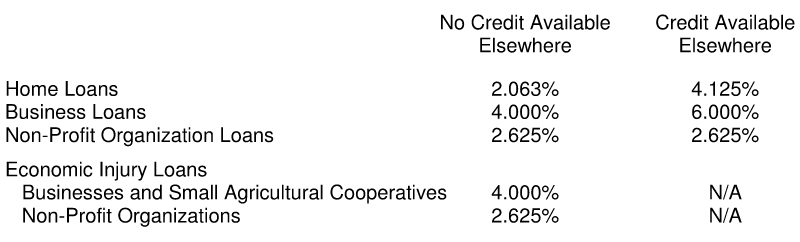

Interest rates can be as low as 2.063 percent for homeowners and renters, 2.625 percent for private nonprofit organizations and 4 percent for businesses, with terms up to 30 years. Loan amounts and terms are set by SBA and are based on each applicant’s financial condition.

Applicants may apply online using the Electronic Loan Application (ELA) via SBA’s secure Web site at

https://disasterloan.sba.gov/ela.Disaster loan information and application forms are also available from SBA’s Customer Service Center bycalling (800) 659-2955 or e-mailing disastercustomerservice@sba.gov. Individuals who are deaf or hard-of-hearing may call (800) 877-8339. For more information about SBA’s disaster assistance programs, visit http://www.sba.gov/disaster.

The filing deadline to return applications for property damage is December 22, 2014. The deadline to return economic injury applications is July 22, 2015. U.S. SBA media release

FACT SHEET – DISASTER LOANS HAWAII Declaration #14165 & 14166

Whether you rent or own your home, own a business, or a small agricultural cooperative located in a declared disaster area, and are the victim of a disaster, you may be eligible for financial assistance from the U. S. Small Business Administration (SBA).

What Types of Disaster Loans are Available?

- Home Disaster Loans – Loans to homeowners or renters to repair or replace disaster-damaged real estate or personal property owned by the victim. Renters are eligible for their personal property losses, including automobiles.

- Business Physical Disaster Loans – Loans to businesses to repair or replace disaster-damaged property owned by the business, including real estate, inventories, supplies, machinery and equipment. Businesses of any size are eligible. Private, non-profit organizations such as charities, churches, private universities, etc., are also eligible.

- Economic Injury Disaster Loans (EIDL) – Working capital loans to help small businesses, small agricultural cooperatives, small businesses engaged in aquaculture, and most private, non-profit organizations of all sizes meet their ordinary and necessary financial obligations that cannot be met as a direct result of the disaster. These loans are intended to assist through the disaster recovery period.

- EIDL assistance is available only to entities and their owners who cannot provide for their own recovery from non-government sources, as determined by the U.S. Small Business Administration.

What are the Credit Requirements?

- Credit History – Applicants must have a credit history acceptable to SBA.

- Repayment – Applicants must show the ability to repay all loans.

- Collateral – Collateral is required for physical loss loans over $14,000 and all EIDL loans over $25,000. SBA takes real estate as collateral when it is available. SBA will not decline a loan for lack of collateral, but requires you to pledge what is available.

What are the Interest Rates?

By law, the interest rates depend on whether each applicant has Credit Available Elsewhere. An applicant does not have Credit Available Elsewhere when SBA determines the applicant does not have sufficient funds or other resources, or the ability to borrow from non-government sources, to provide for its own disaster recovery. An applicant, which SBA determines to have the ability to provide for his or her own recovery is deemed to have Credit Available Elsewhere. Interest rates are fixed for the term of the loan. The interest rates applicable for this disaster are:

What are Loan Terms?

The law authorizes loan terms up to a maximum of 30 years. However, the law restricts businesses with credit available elsewhere to a maximum 7-year term. SBA sets the installment payment amount and corresponding maturity based upon each borrower’s ability to repay.

What are the Loan Amount Limits?

- Home Loans – SBA regulations limit home loans to $200,000 for the repair or replacement of real estate and $40,000 to repair or replace personal property. Subject to these maximums, loan amounts cannot exceed the verified uninsured disaster loss.

- Business Loans – The law limits business loans to $2,000,000 for the repair or replacement of real estate, inventories, machinery, equipment and all other physical losses. Subject to this maximum, loan amounts cannot exceed the verified uninsured disaster loss.

- Economic Injury Disaster Loans (EIDL) – The law limits EIDLs to $2,000,000 for alleviating economic injury caused by the disaster. The actual amount of each loan is limited to the economic injury determined by SBA, less business interruption insurance and other recoveries up to the administrative lending limit. SBA also considers potential contributions that are available from the business and/or its owner(s) or affiliates.

- Business Loan Ceiling – The $2,000,000 statutory limit for business loans applies to the combination of physical, economic injury, mitigation and refinancing, and applies to all disaster loans to a business and its affiliates for each disaster. If a business is a major source of employment, SBA has the authority to waive the $2,000,000 statutory limit.

What Restrictions are there on Loan Eligibility?

- Uninsured Losses – Only uninsured or otherwise uncompensated disaster losses are eligible. Any insurance proceeds which are required to be applied against outstanding mortgages are not available to fund disaster repairs and do not reduce loan eligibility. However, any insurance proceeds voluntarily applied to any outstanding mortgages do reduce loan eligibility.

- Ineligible Property – Secondary homes, personal pleasure boats, airplanes, recreational vehicles and similar property are not eligible, unless used for business purposes. Property such as antiques and collections are eligible only to the extent of their functional value. Amounts for landscaping, swimming pools, etc., are limited.

- Noncompliance – Applicants who have not complied with the terms of previous SBA loans are not eligible. This includes borrowers who did not maintain flood and/or hazard insurance on previous SBA or Federally insured loans.

Is There Help with Funding Mitigation Improvements?

If your loan application is approved, you may be eligible for additional funds to cover the cost of improvements that will protect your property against future damage. Examples of improvements include retaining walls, seawalls, sump pumps, etc. Mitigation loan money would be in addition to the amount of the approved loan, but may not exceed 20 percent of total amount of physical loss, as verified by SBA to a maximum of $200,000 for home loans. It is not necessary for the description of improvements and cost estimates to be submitted with the application. SBA approval of the mitigating measures will be required before any loan increase.

Is There Help Available for Refinancing?

- SBA can refinance all or part of prior mortgages that are evidenced by a recorded lien, when the applicant (1) does not have credit available elsewhere, (2) has suffered substantial uncompensated disaster damage (40 percent or more of the value of the property), and (3) intends to repair the damage.

- Homes – Homeowners may be eligible for the refinancing of existing liens or mortgages on homes, in some cases up to the amount of the loan for real estate repair or replacement.

- Businesses – Business owners may be eligible for the refinancing of existing mortgages or liens on real estate, machinery and equipment, in some cases up to the amount of the loan for the repair or replacement of real estate, machinery, and equipment.

What if I Decide to Relocate?

You may use your SBA disaster loan to relocate. The amount of the relocation loan depends on whether you relocate voluntarily or involuntarily. If you are interested in relocation, an SBA representative can provide you with more details on your specific situation.

Are There Insurance Requirements for Loans?

To protect each borrower and the Agency, SBA may require you to obtain and maintain appropriate insurance. By law, borrowers whose damaged or collateral property is located in a special flood hazard area must purchase and maintain flood insurance for the full insurable value of the property for the life of the loan.U.S. SBA media release

by Big Island Video News

on at

STORY SUMMARY

Low-interest federal disaster loans will be available "to homeowners, renters, and businesses of all sizes.